If you’re feeling overwhelmed managing your finances and don’t where to start, simple frameworks like the 50/30/20 rule can help you take control and take the stress out of budgeting. It won’t solve every financial challenge, but it does offer a simple way to see where your money is going — and where you might have more control than you think. This guide explains how it works and, just as importantly, what to do if the numbers don’t add up the way they’re supposed to.

What is the 50/30/20 rule?

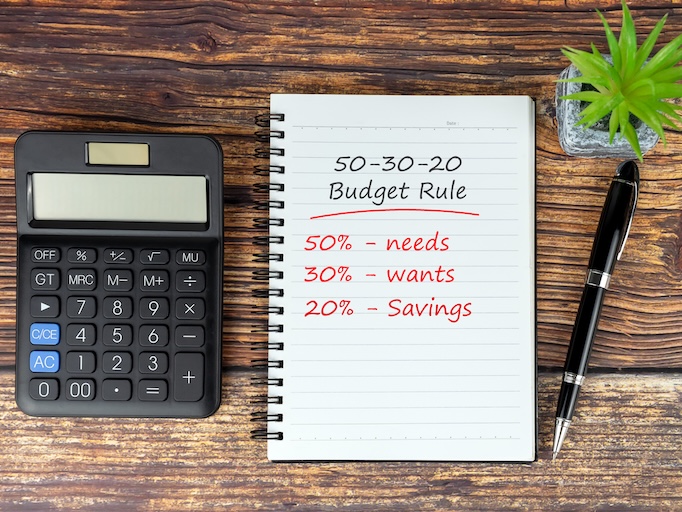

At its core, the 50/30/20 rule is a budgeting method that divides your after-tax income into three broad categories:

- 50% for needs

- 30% for wants

- 20% for savings or debt repayment

This approach is widely recognised as a straightforward way to balance spending and saving. Financial organisations such as HSBC and Bank of Scotland describe it as a simple framework to help manage money more effectively and stay in control of your finances.

Rather than tracking every pound, the rule focuses on the bigger picture. It gives you clear boundaries while still allowing flexibility, something that’s especially valuable when life (and costs) change.

The key components of the 50/30/20 rule

At its most basic it’s a way of categorising your expenditure with some benchmarks to help you get control over your finances. Understanding what falls into each category is essential. While the percentages stay the same, the details will vary depending on your lifestyle and priorities.

1. Needs (50%)

“Needs” are your essential expenses, the costs you can’t avoid. These are the foundations of your day-to-day life.

Typical examples include:

- Rent or mortgage payments

- Utility bills (gas, electricity, water)

- Basic groceries

- Transport costs (commuting, fuel)

- Insurance and minimum debt repayments

These tend to be your largest expenses, which is why they’re allocated the biggest share of your budget.

If your needs exceed 50%, you’re not alone, particularly in higher-cost areas like London. In these cases, the rule can be adjusted temporarily while you look for ways to reduce fixed costs over time.

2. Wants (30%)

Wants are the things that make life enjoyable but aren’t strictly necessary. They’re flexible and can be adjusted more easily if needed.

Examples include:

- Eating out or takeaway meals

- Holidays and travel

- Streaming subscriptions or memberships

- Shopping and entertainment

- Hobbies and leisure activities

The key here is balance. The 50/30/20 rule doesn’t eliminate fun spending, it simply keeps it within a manageable limit. This is one of the reasons the method is so popular: it avoids the “all or nothing” approach that can make budgeting feel restrictive.

3. Savings and debt (20%)

The final 20% is all about your financial future. This category helps you build resilience and long-term security.

It can include:

- Emergency savings

- Pension contributions

- Investments (such as ISAs)

- Overpayments on loans or credit cards

- Saving for specific goals (e.g. deposit for a home)

If saving 20% feels out of reach, that’s a reasonable place to be – especially with so many costs rising. Saving small amounts can make a significant difference over time.

Paying down debts regularly every month can help you become debt free over time and help to build your credit profile which may make borrowing easier for ‘future you’.

Why the 50/30/20 rule works

There are countless budgeting methods out there, but the 50/30/20 rule stands out for its simplicity and flexibility.

Here’s why many people find it effective:

- It’s easy to understand: no complex calculations or detailed tracking required

- It creates balance: covering essentials, lifestyle and future goals in one framework

- It’s adaptable: you can tweak the percentages to suit your situation

- It encourages consistency: regular saving becomes part of your routine

Research and financial guidance suggest that structured budgeting approaches like this can help people save more consistently and feel more in control of their finances.

How to apply the 50/30/20 rule

Getting started with the 50/30/20 rule is straightforward. You don’t need specialist tools, just a clear view of your income and spending.

Step 1: Work out your take-home income

Focus on your net income (after tax, National Insurance and pension contributions). This is the amount you actually have available to spend.

Step 2: Categorise your spending

Review your current expenses and group them into:

- Needs

- Wants

- Savings/debt

This step can be eye-opening. Many people find they’ve been classifying “wants” as “needs” without realising it.

Step 3: Calculate your percentages

Work out how your spending compares to the 50/30/20 split. For example:

- If you earn £2,500 per month:

- £1,250 for needs

- £750 for wants

- £500 for savings

Step 4: Adjust where needed

If your spending doesn’t match the rule, that’s completely normal. The aim isn’t perfection, but progress.

You might:

- Reduce discretionary spending

- Look for ways to lower fixed costs

- Increase your savings rate gradually

Step 5: Automate where possible

Setting up automatic transfers to savings can make the process much easier. Many banks also offer budgeting tools and spending insights to help you stay on track.

Making the rule work in real life

While the 50/30/20 rule is a great starting point, it isn’t one-size-fits-all. Your version of the rule should reflect your personal circumstances.

Some common adjustments include:

- Higher living costs: You might spend closer to 60% on needs and reduce wants temporarily

- Debt repayment focus: You may increase the 20% allocation to pay down debt faster

- Lower income: Prioritising essentials first, then building savings gradually

- Irregular income: Using an average income over several months

The key is to treat the rule as a guide rather than a strict formula. Feel free to adjust and review every month to find out what works for you at this time, the goal is to support your financial wellbeing, not create unnecessary pressure.

Common challenges (and how to overcome them)

Like any budgeting method, the 50/30/20 rule comes with a few challenges , but they’re usually manageable with small adjustments and the right support.

High essential costs:

Rising housing, energy and food costs can push “needs” well beyond the recommended 50%, particularly for those living in more expensive areas. If this happens:

- Focus first on reducing discretionary spending where possible

- Review bills and subscriptions to identify potential savings

- Consider switching providers or negotiating better deals

Inconsistent income:

If your income varies from month to month (for example, if you’re self-employed or freelance), sticking to fixed percentages can be tricky. You could:

- Base your budget on an average income over several months

- Build a financial buffer during higher-earning periods

- Prioritise essential costs first, then allocate the rest flexibly

Struggling to save 20%:

Setting aside 20% of your income may feel unrealistic, especially if you’re already stretched. In this case:

- Start with a smaller, manageable amount, even 5–10% is a positive step

- Increase your contributions gradually over time

- Focus on building an emergency fund first for added security

Feeling overwhelmed or unsure where to start:

For many people, the biggest challenge isn’t the numbers, it’s knowing how to take control of their finances in the first place. If you’re finding budgeting difficult or feeling under financial pressure, it’s important to know that support is available.

Fair Finance offers a free and accessible money advice tool designed to help you better understand your financial situation, explore your options and take practical steps towards improving your finances. It can be a helpful starting point if you’re unsure how to apply budgeting methods like the 50/30/20 rule in your own circumstances.

Alternatively, free and impartial advice is available through MoneyHelper, a government-backed service. They provide guidance on dealing with debt, managing money and accessing support services. Their debt advice locator can connect you with regulated organisations offering confidential help with debt counselling, debt adjustment and credit information.

Whichever route you choose, reaching out for support can make a real difference. Budgeting frameworks like the 50/30/20 rule are most effective when combined with trusted guidance and tools that help you stay on track.

This article is for information purposes only.